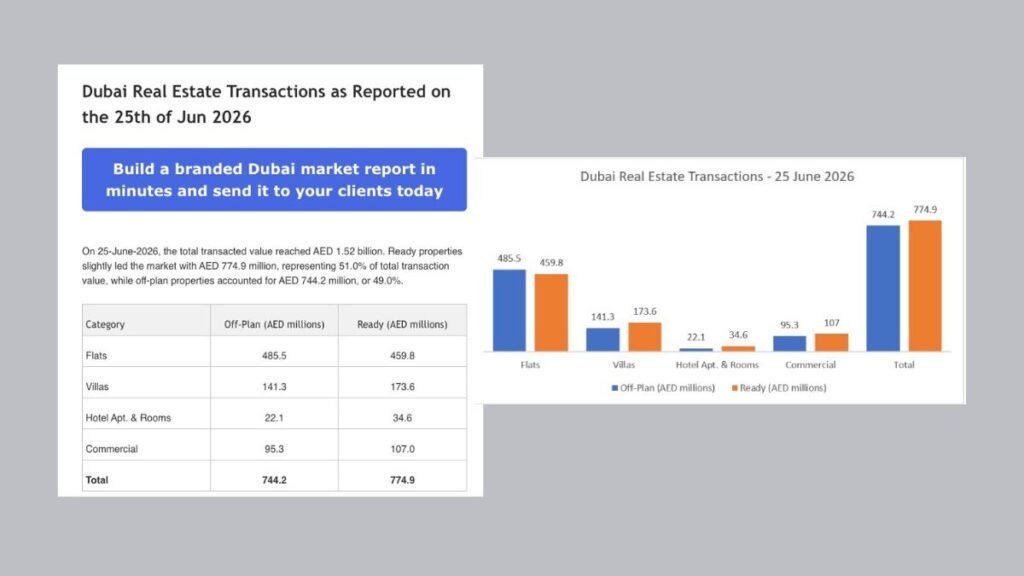

Dubai, UAE — Completed homes outsold off-plan launches in Dubai on 25 June, taking AED 774.9 million in deals against AED 744.2 million for under-construction stock on a day when total residential and commercial transactions reached AED 1.52 billion. The 51% ready, 49% off-plan split by value runs against the pattern that has shaped the city through 2026, when new launches have carried most of the activity.

Ready stock edges off-plan on a AED 1.52 billion day

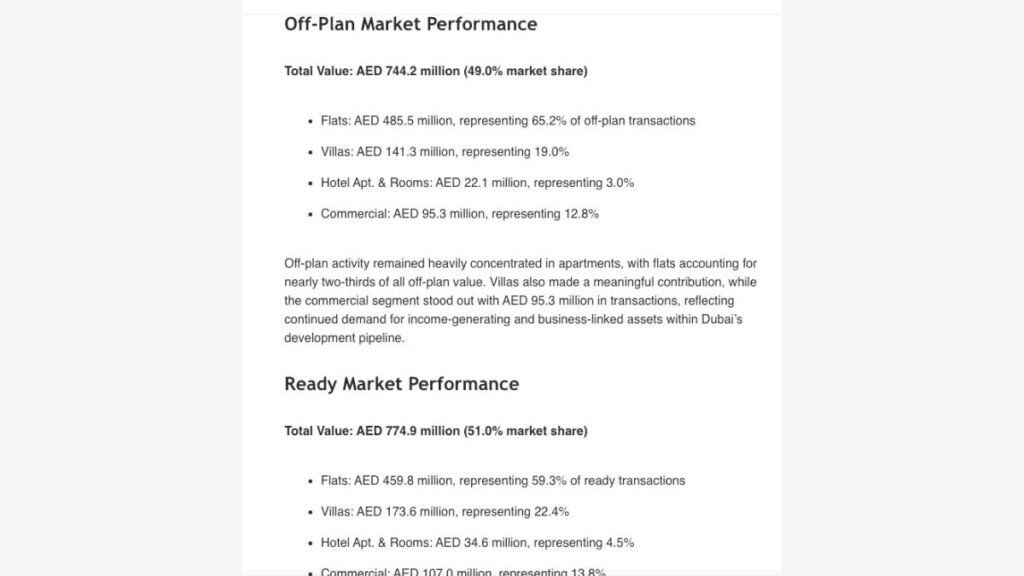

Through the first quarter, off-plan property accounted for roughly 70% of Dubai’s residential transaction value and about 72% of volume, on Savills figures compiled from Dubai Land Department data. Off-plan sales climbed 9.4% year-on-year over that window while ready-market transactions fell 8.0%. Against that backdrop, a day where completed homes pull ahead breaks the recent run. Flats did the heavy lifting on both sides of the ledger, at AED 485.5 million off-plan and AED 459.8 million ready, with commercial assets adding AED 95.3 million and AED 107.0 million respectively.

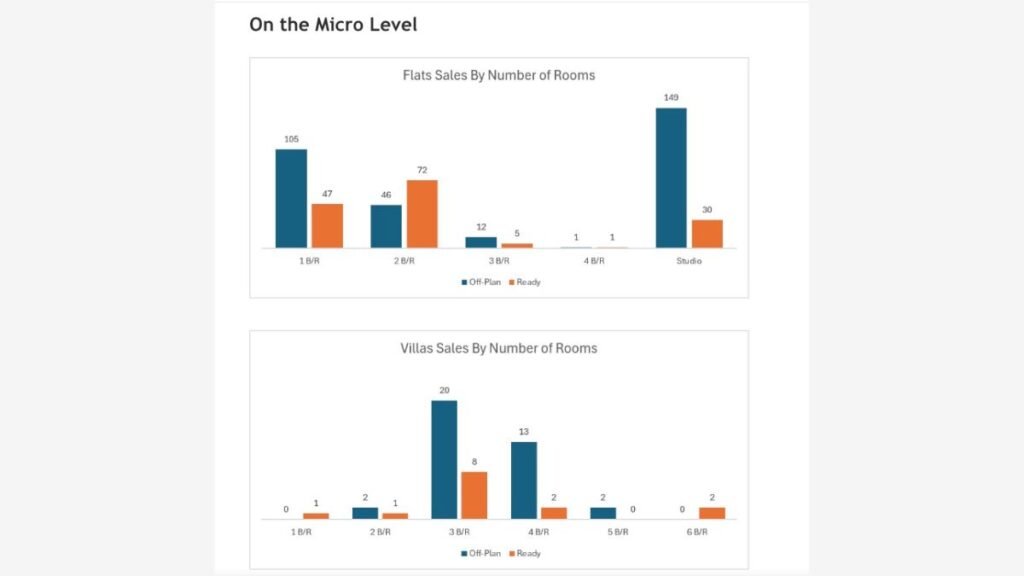

149 studios and 105 one-beds carry the off-plan book

The unit mix separates two buyer pools. Off-plan flat sales clustered at the small end, with 149 studios and 105 one-bedroom units changing hands against 46 two-bed and 12 three-bed deals. Ready flats leaned the other way: two-bedroom units led at 72 sales, one-beds at 47. Villas told a comparable story, with three-bedroom homes leading both segments while off-plan villa demand ran ahead across the larger four- and five-bedroom formats.

That distribution maps onto how each market is bought. Studios and one-beds are the yield instruments, lower in ticket, faster to let, the entry point for an investor building rental income. Larger ready units draw families and end-users who want to occupy now rather than wait two or three years for a handover date. The day did not pit one market against the other so much as show them serving different customers at the same time.

Why the split matters for an NRI weighing yield against occupancy

For an overseas buyer, the practical question is whether to chase pre-launch pricing or pay for an asset that earns from day one. Indian nationals stayed Dubai’s largest foreign buyer group through 2025, at close to a fifth of recorded activity, pulled by gross rental yields in the 6 to 9% range in mature districts and the absence of property or capital gains tax. Indian investors also work within the Reserve Bank of India’s Liberalised Remittance Scheme, which caps outward remittance at USD 250,000 per person each financial year, so larger purchases often mean pooling family limits. Off-plan still offers staged payment plans and entry prices below comparable ready stock; completed property removes construction risk and starts paying rent at once. The 25 June sheet shows both routes taken in volume on the same day.

The day looked less like a turning point than like both markets working at once: off-plan drawing investors who want pre-launch pricing and a payment runway, ready stock drawing buyers who value immediate occupancy and rent. Dubai has leaned on new launches to carry volume for three years, yet completed homes still clear in size when the buyer wants certainty over upside. For an NRI choosing between the two, the day is a useful reminder that both routes remain liquid.

Whether the ready tilt holds is a question for the weekly data

One day is not a trend, and the read worth watching is whether ready demand holds through the rest of June or eases back as off-plan launches resume. Equally open is where the completed-home buying concentrated: a tilt led by Dubai Marina and Downtown apartments would point to appetite for prime ready stock, while a villa-led surge in the suburbs would tell a different story about family relocation. The nationality mix behind the day, and how much of the ready buying was mortgage-backed rather than cash, will shape whether this reading sharpens into a Q3 pattern. Those are the threads to follow in the coming weekly numbers.

A 120,000-unit handover year still weighs on ready pricing

The larger risk sits in supply. Around 120,000 units are scheduled for handover across Dubai in 2026 on DLD pipeline data, a wave likely to keep pressure on prices and rents in the completed market as stock arrives. March was a reminder of how fast sentiment can move: transaction value fell 28.8% month-on-month to AED 43.7 billion, with the ready segment among the most exposed, according to Mira International, which tied the drop to regional tensions and seasonal factors. A day where ready property leads is welcome for sellers of finished homes, but it does nothing to clear the inventory overhang, and prices in the segment are likely to stay sensitive rather than firm decisively while delivery runs at this pace.

Discover more from Invest Dubai Today - Dubai Realty Insights

Subscribe to get the latest posts sent to your email.